We’ve said it before, and we’ll say it again: nobody moves markets like Mario Draghi.

The euro gained 2.5% on the dollar today (Dec. 3)—an absolutely enormous move. Some $5 trillion is traded in currency markets every day, and the euro-dollar trade accounts for around a quarter of that volume. A move like the one today is very rare in a market with that sort of vast liquidity.

What happened?

After Draghi, the president of the European Central Bank, dropped hints last month that he was open to boosting the bank’s stimulus measures to support the economy, markets figured that “Super Mario” was laying the groundwork for some monetary shock and awe at the ECB’s regularly scheduled meeting today.

As it happened, Draghi disappointed investors with moves that were less aggressive than expected. Among other measures, the ECB cut one of its key interest rates further into negative territory (from -0.2% to -0.3%) and extended its program of buying €60 billion in government bonds every month through at least March 2017 (from September 2016).

These sorts of actions generally push down the value of the euro—a good thing for the euro-zone economy these days. A weaker euro boosts growth by making exports from the euro zone more competitive abroad, while it also pushes up prices at home, which guards against the region’s long and dangerous flirtation with deflation. Indeed, the euro has fallen by more than 10% against the dollar so far this year, and 20% over the past two years.

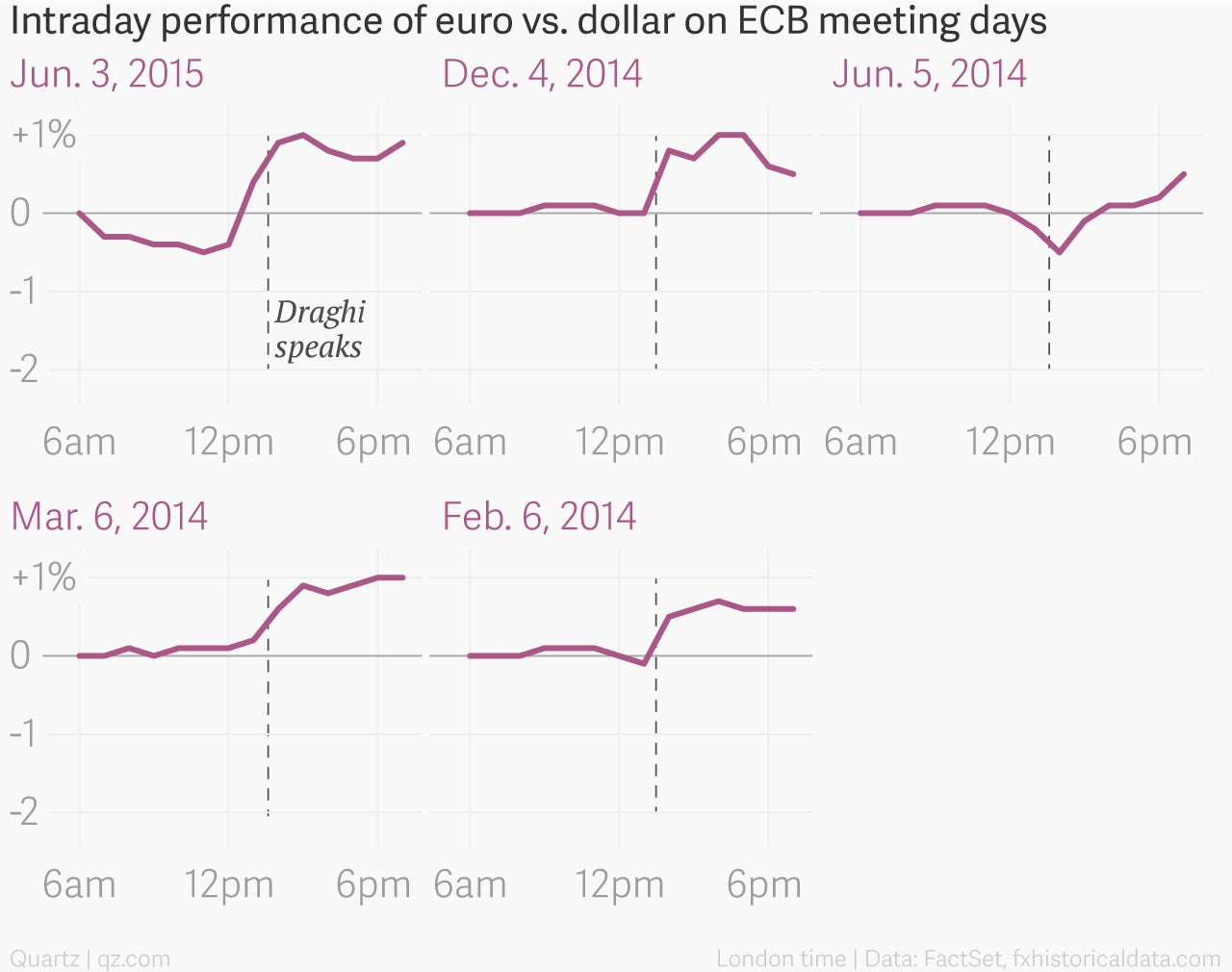

But when the markets think that even more forceful actions are required to break the euro zone out of its stupor—bigger rate cuts, bolder bond purchases—you get a sharp and unexpected move in the opposite direction, like the one today. It isn’t the first time that Draghi’s has sent the euro higher with his comments after an ECB rate-setting meeting, but it is by far the largest in scale:

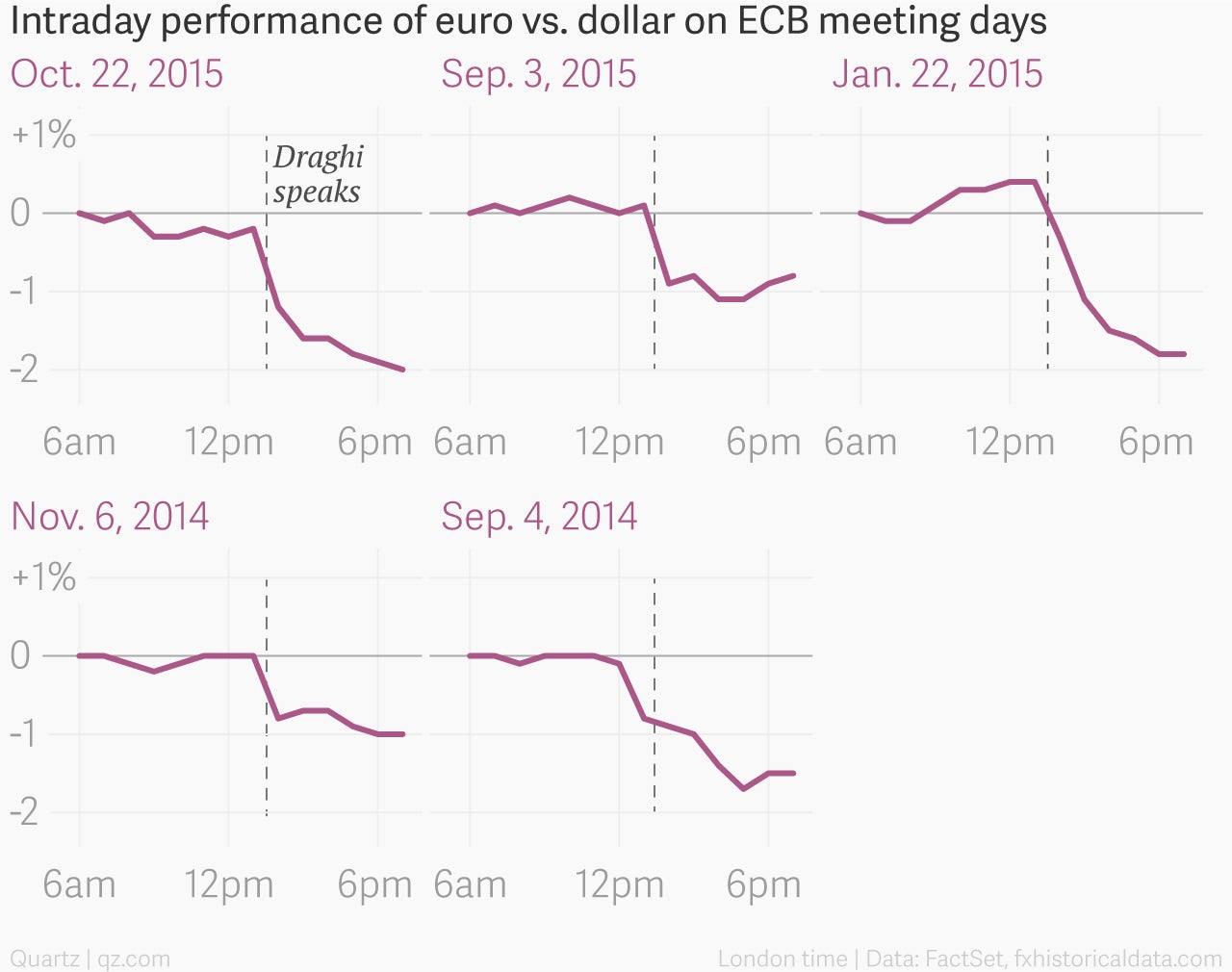

More common recently have been sharp drops in the euro when Draghi took the mic, which might explain why so many traders were caught so badly off-guard:

Why did Draghi disappoint? The ECB’s own economic projections aren’t exactly rosy, with GDP forecasts for the next two years lower today than shortly after the central bank started buying government bonds in January:

And inflation is nowhere near the ECB’s target of 2%, with the bank’s latest forecasts showing inflation drifting even further from this goal than at the start of the year:

For this reason, Draghi told reporters, a “very large majority” of the ECB’s governing board reckoned that more stimulus was needed. “We are doing more because it works,” Draghi said, noting that the forecasts for both inflation and GDP would be even grimmer if not for the bank’s efforts to date.

But could things be even better with more aggressive action? The markets have certainly think so.