It’s been a banner year for financial scams in China. Prominent among them was Fanya Metal Exchange—wringing $6 billion or so from duped investors—but it certainly wasn’t alone. Chinese investors lost about $24 billion to such chicanery this year. Many risked their entire life savings, regardless of unrealistic assurances of zero risk, or promises of high returns that should have sounded too good to be true. Following, a look back at this year’s “highlights,” and some expert analysis on why so many fell for empty promises.

It’s been a banner year for financial scams in China. Prominent among them was Fanya Metal Exchange—wringing $6 billion or so from duped investors—but it certainly wasn’t alone. Chinese investors lost about $24 billion to such chicanery this year. Many risked their entire life savings, regardless of unrealistic assurances of zero risk, or promises of high returns that should have sounded too good to be true. Following, a look back at this year’s “highlights,” and some expert analysis on why so many fell for empty promises.

Fanya Metal Exchange—about $6 billion

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

This week (Dec. 22) in Kunming the local government announced (link in Chinese) the launch of investigations into this infamous “trading platform,” which fleeced hundreds of thousands of investors and froze $6 billion in investor cash in April.

Awkwardly enough the local government itself backed Fanya, helping it get set up and officially endorsing it in 2011. Fanya gained more credibility by advertising on state television, which to many viewers conferred a sort official recognition. Some 220,000 investors flocked to Fanya’s flagship “product,” rare metals traded on its electronic platform. The company promised zero risk and an annual return of 13%.

Outcries after the money was frozen prompted arrests of some protesting investors.

As it turns out, the prices and quantities on the exchange—say, for the rare metal indium—were completely disconnected from those in other spot markets, both at home and aboard.

The warehouses where Fanya supposedly stored its metals might never have existed, judging by both analyst observations and an investor’s first-person account. Many people, unsurprisingly, have concluded that the exchange was a Ponzi scheme. The head of Fanya disappeared last week.

E Zubao and other P2P financing platforms—at least $11 billion

Earlier this month, E Zubao, China’s biggest online peer-to-peer lending platform by amount, came under investigation for suspected illegal operations (link in Chinese). Police have seized assets and detained several suspects. Since its launch in mid-2014, the company has lent 70 billion yuan ($10.8 billion) through its financial products, and promised annual returns of between 9% and 14%, reports business magazine Caixin (link in Chinese).

E Zubao wasn’t alone. Many shady players took advantage of China’s largely unregulated P2P lending market. Dada Group, which forces employees to buy its own financial products, was probed by the police days after the investigation into E Zubao.

At the end of last year, nearly a quarter of China’s P2P lenders—then numbering 1,500—had failed. The market was then estimated at 276 billion yuan, as Quartz reported. This year, the number of such platforms reached more than 3,400, and nearly half of them had failed by November, according to industry data provider 01caijing (link in Chinese).

By the time E Zubao went sour, investors had lost an estimated $1.2 billion in P2P lending platforms—most of which were fraudulent—largely since early last year. That’s according to an October report by online financing firm Creditease, which backs Yirendai, the first Chinese online P2P platform listed overseas.

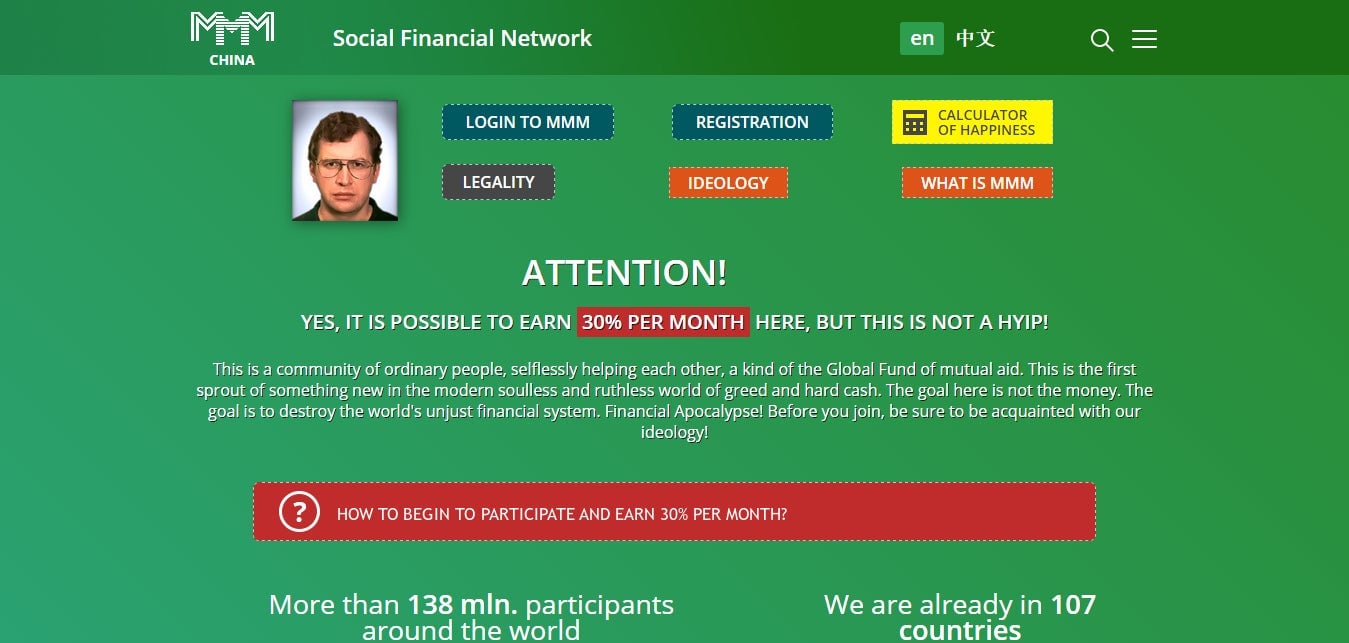

MMM social financial network—beyond calculation

Founded by fraudster Sergey Mavrodi, the notorious MMM social financial network cheated millions of Russians out of their savings in the 1990s. It’s had a rebirth in China and elsewhere.

Bearing the elements of a typical pyramid scheme, MMM promises investors 30% monthly interest (paywall), with bonuses for referrals, and for posting glowing testimonials on its website.

As MMM China requires new participants to buy bitcoins to join, in a recent 30-day stretch it sparked a surge (paywall) of more than 100% in the currency’s price. It’s also inspired many Chinese knockoffs claiming to be “helping each other” online financial platforms.

Money involved in the Chinese version of the scheme is not accountable at the moment—and might never be.

Zhuoda Group—about $1.6 billion

Zhuoda Group, a fast-growing property developer that claims it can build 3D-printed houses, has raised about 10 billion yuan ($1.6 billion) from over 400,000 Chinese investors by selling financial products that guarantee annual returns as high as 30%. But its financial products don’t have any underlying assets to support those returns, according to the digital publication Watching (partly owned by Alibaba), and the company claims overseas deals with nonexistent parties. The local Hebei provincial government has launched investigations into Zhuoda’s fundraising in response to Watching’s reports, but has not yet revealed its findings.

GSM Financial Group—about $6.2 billion

GSM Financial Group markets itself as a foreign exchange agency licensed by the Australian Securities and Investments Commission, with offices around the world. It appears to be a typical pyramid scheme.

Investors—with a minimum investment of $2,000—are guaranteed a monthly return of 8% in 18 months, and another 8% commission from the “downlines” they develop, reported the Guangzhou-based paper Yangcheng Evening News in April (link in Chinese). GSM has bilked an estimated 40 billion yuan ($6.2 billion) from investors across the country since it began appearing at financial expos in April 2014. The police launched an investigation into GSM a year later.

The operation cannot be found at the Shenzhen address it used to register with the State Administration for Industry and Commerce (link in Chinese).

Amid the country’s slowest growth in over a decade, Chinese investors—including the world’s now-biggest middle class—are looking for places to put their money besides low-interest banks, the volatile stock market, or the collapsing property market. This is often a starting point when dissecting the reasons why so many Chinese fall for schemes.

Insufficient regulation in China’s financial markets also contributes to the tragedies. Under the national leaders’ push for financial reform, mistakes seem to be tolerable in the name of innovation. When new investment opportunities are created in China, supervision often comes afterwards.

With many regional firms and exchanges that turned out to be frauds—exemplified by Fanya—the de facto supervisors are the financial divisions of local governments. The involved authorities often back the launch of such companies, or consider them too valuable to lose.

Online P2P lending platforms, for their part, should act solely as information brokers (more or less matchmakers) under the ambiguous regulations. But many stepped out of line by providing services and products that only licensed banks or lending companies may offer.

As for the numerous financial platforms that are not even registered with the State Administration for Industry and Commerce, many “don’t have any qualifications, but cannot be supervised,” Tang Jihe, a precious metals analyst who follows Fanya, told Quartz on the condition that his employer not be named. “Authorities will mostly pass the buck to each other.”

But what about from an investor’s point of view? ”Chinese laobaixing [ordinary people] are like a swarm of bees,” Tang said. When faced with temptation, “even experienced investors will think irrationally.”

With China’s economic activities dominated by state-backed institutions, Chinese investors generally expect governments of different levels to have their backs in the event of a scandal, Michael Wong, associate professor of finance at City University of Hong Kong, told Quartz. ”Such expectations result in moral hazard… investors do not pay much attention to the risk of investment schemes.”

Most savvy investors from Hong Kong or Taiwan would never believe in financial products that promised “guaranteed revenues”—even if they were offered by banks. By contrast, many mainland Chinese investors have a “deep-rooted perception” that a bank (or what if offers) could never fail, said Lu Tsung, an investment analyst with Shanghai-based Jiujiu Internet Financial Services, in an interview with Quartz. (Lu has worked for both a P2P lender and a state-owned bank.)

In other cases, investors “just play around with the system, what we call fishing,” Li Kui Wai, an associate professor at City University of Hong Kong, told Quartz. Investors in developed countries also want to make money, but many Chinese investors are just greedy, said Li, who specializes in China’s financial development. Even if they don’t trust a system or platform, “they are happy to make quick money [in it]. We just fish around. If you get a big fish, well, good luck. If you are being fished, then too bad.”

At the end of the day, what China needs to do is build more trustworthy financial systems, believes Wong. It should not, however, expect that investors will make better decisions.