It is an “island of stability.” It is stronger than its main rivals. All hail the euro, king of currencies.

It is an “island of stability.” It is stronger than its main rivals. All hail the euro, king of currencies.

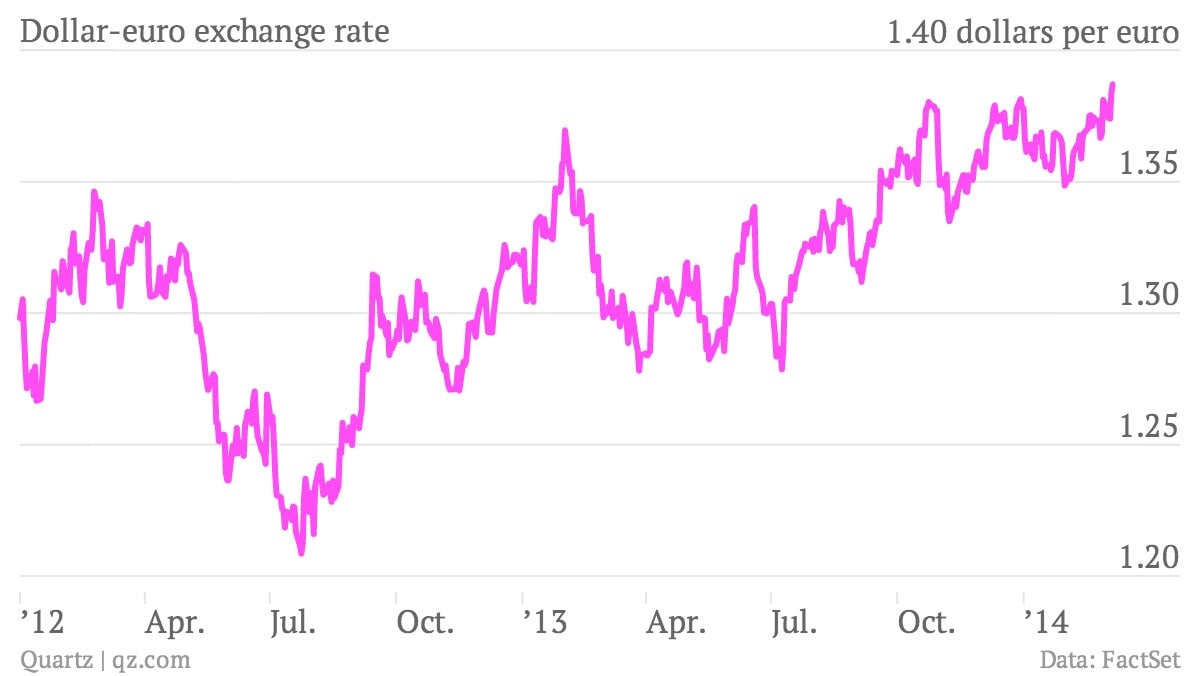

The euro set a two-year high against the dollar today. From its low in mid-2012, it has gained 15% against the greenback and almost 50% against the yen. What gives?

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Mario Draghi, president of the European Central Bank, coined the “island of stability” term at a press conference yesterday, after the bank left rates unchanged and published a relatively upbeat set of economic forecasts. This convinced traders that the central bank won’t loosen monetary policy any time soon, despite the pressure to act from several corners. This stands in contrast to the US Federal Reserve, which is only gradually tapering its stimulus, and the Bank of Japan, which keeps revving its printing presses. If by “stability” Draghi meant inaction, then the ECB’s do-nothing strategy has, somewhat perversely, seen the euro gain ground on other currencies.

The recent economic data out of the euro zone also suggests that the monetary union’s darkest days might be behind it. Euro-zone purchasing managers are as bullish as they have been in two-and-a-half years. German factories are humming, Spanish exports are rising, and even some numbers from Greece are not half bad. To the extent that a strong euro reflects brighter economic prospects, policymakers will be happy if the currency goes up even more, as some expect it will.

But the euro’s strength won’t help boost the euro zone’s perilously low inflation rate. At his press conference, Draghi said that the euro’s ascent over the past two years has lowered inflation by 0.4 percentage points. And that was before the currency jumped even higher after his remarks. Some have semi-seriously tried to reverse-engineer Draghi’s claim based on the latest exchange rate, which suggests that if not for the euro’s strength, inflation in the euro zone, currently 0.8%, would be much closer to the ECB’s 2% target.

Can the euro keep this up? Euro-zone GDP is expected to grow by just over 1% this year, which is hardly a world-beating performance. Much will depend, then, on the actions of others; in recent months, relief that the euro zone finally (probably) dragged itself out of the economic doldrums, combined with the ECB’s intransigence on interest rates and monetary stimulus, has made the euro the least ugly option out there for currency traders. To quote Kris Kristofferson, as certain fund managers are wont to do, it is the “cleanest dirty shirt” of the major currencies.