Things are going haywire in China. Earlier this week, markets were blindsided by jarringly low February lending, prompting fears that tightening by the central bank, the People’s Bank of China, would throttle growth. On top of that, abysmal export data suggested growth may already have begun withering. Global stock markets are convulsing. And while copper cratered yesterday, hitting a 44-month low, iron ore lost 8.3%, its biggest single-day loss in four years.

Things are going haywire in China. Earlier this week, markets were blindsided by jarringly low February lending, prompting fears that tightening by the central bank, the People’s Bank of China, would throttle growth. On top of that, abysmal export data suggested growth may already have begun withering. Global stock markets are convulsing. And while copper cratered yesterday, hitting a 44-month low, iron ore lost 8.3%, its biggest single-day loss in four years.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

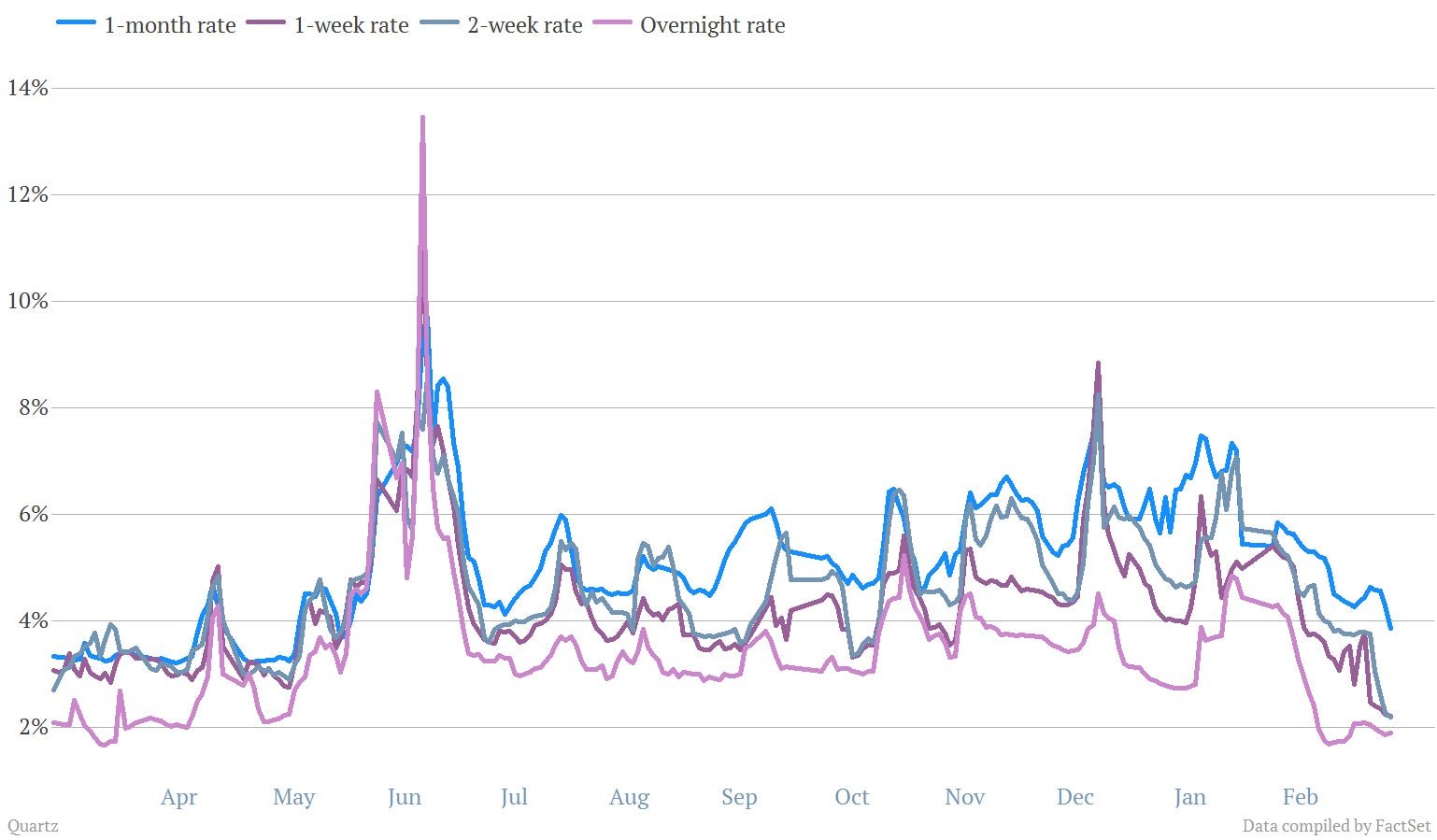

Not everyone is panicking. Take, for instance, Chinese banks. Interbank rates have slipped lower than they’ve been in nearly a year, signaling that the liquidity problems dogging the PBoC since June 2013 have, at least for the moment, subsided:

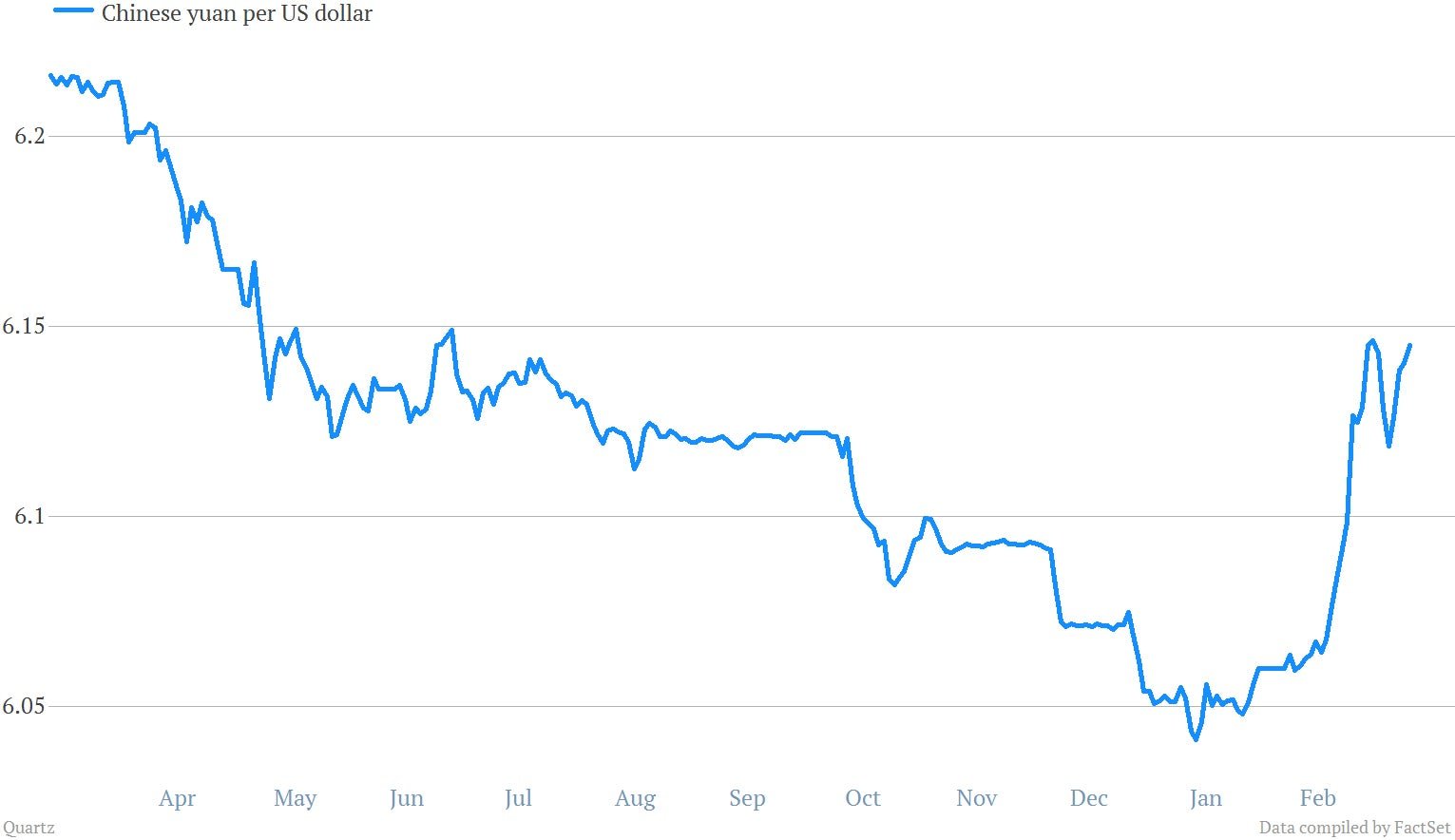

Economists think both the good news and the bad news have something in common: the epic slide of the yuan against the dollar. Here’s why:

The PBoC sets the value of the yuan versus the dollar each day, letting it swing 1% in either direction. Since China runs such a huge current-account surplus, it’s natural to assume the PBoC will have to let its currency gradually strengthen. An easy way to bet on that is by borrowing dollars or yen outside mainland China—often in Hong Kong—exchanging those for yuan, and investing them onshore. Last year, that trade pumped $500 billion in “hot money,” as this speculative cash is called, over China’s borders.

Since this often flows into already bubbly property or risky off-balance-sheet lending system known as “shadow credit,” the government is generally not a big fan. The PBoC gets extra-angsty about having to subsidize these hot money profits, which it ends up doing by preventing the yuan from strengthening as much as it might otherwise.

Since Feb. 17, the PBoC has pushed the yuan to lose 1.3% against the dollar, nearly half of what it gained in 2013. Though only China’s leaders know what’s really behind this move, one objective almost certainly is blocking traders—most of them domestic companies and banks—from profiting on speculative bets that the yuan will strengthen against the dollar.

Once it became clear that the PBoC wasn’t messing around, a collective cheapening-yuan freakout set in. Speculators scrambled to settle their trades, says Andrew Polk, an economist at the Conference Board, compounding the rush out of yuan and into dollars.

“The PBoC changed the calculus on everyone by suddenly devaluing the renminbi [another name for the yuan],” he says. “Basically that means the dollars speculators borrowed [for investment positions betting that the yuan would strengthen] are now more expensive and some are coming due, so suddenly the dollar has become much more precious.”

Last June, the PBoC inadvertently plugged up a channel through which hot money was flowing into China. That was a big factor behind the cash crunch that month, which saw the one-week interbank rate—what banks charge each other—leap to a terrifying 12%. Money stopped flowing; liquidity seized.

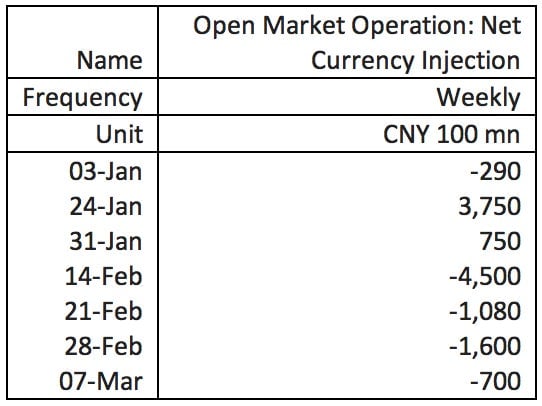

So you’d think that by killing the hot money inflows, the PBoC would cause a similar liquidity crisis—particularly given that the PBoC has been draining money like crazy. But nope. To the contrary, liquidity is looser than it has been in eons. The one-week interbank rate is now at 2.21%, a low it hasn’t hit since May 2012.

One reason is, paradoxically, the PBoC’s yuan-tweaking, says Polk. ”The reason the interbank rates spiked [in June and December] was due to sudden, and now often, strong renminbi demand,” he says. “You sort of have the opposite currently—the trade is reversed. Domestic corporates and domestic banks appear to be selling renminbi to buy dollars onshore, so the market is flooded with renminbi liquidity. So far this doesn’t appear to have sparked significant RMB outflow (which would push up interbank rates), but is causing a reallocation from RMB to USD both on and offshore.”

It’s unlikely to be just the dollar-buying of Chinese companies and banks that’s suppressing rates, though. The PBoC may be supporting banks behind the scenes, says Amy Yuan Zhuang of Nordea, a research firm. The PBoC would probably need to throw some sop to banks to encourage cooperation, given that many undoubtedly lost money due to the yuan’s weakening.

Another likely factor is the rapid growth of Alibaba’s Yu’e Bao and other internet money-market funds, says Nicholas Borst of Peterson Institute of International Economics, explaining that since these products invest mostly in interbank products, they add to the supply of funds.

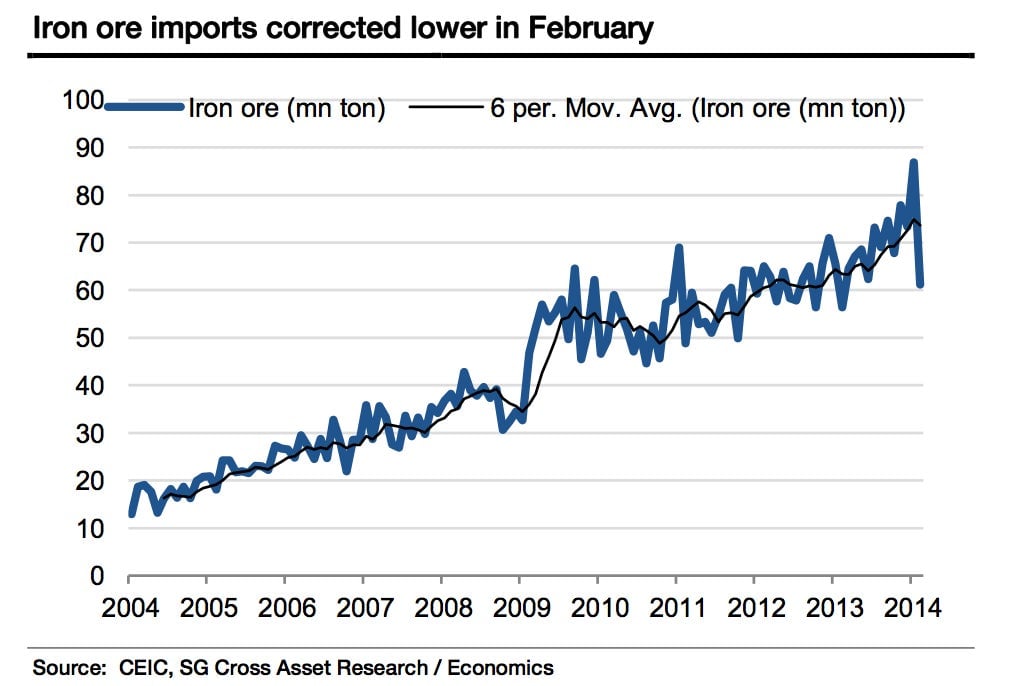

Chinese metal traders have long imported copper and iron ore as collateral for onshore loans, profiting both from the yuan’s strengthening and from high onshore interest rates. And sometimes they also profit from using the same pile of metal to take out multiple loans.

In fact, as much as 60-80% of China’s imported copper is used as collateral for loans. And since most of that was bought priced in dollars, and will be sold back onto the global market in dollars, the yuan’s weakening makes those dodgy traders lose money. When the yuan kept weakening, traders panicked and sold out of their positions, cutting their losses in order to pay back loans, says Nordea’s Yuan.

The fact that the week-long Chinese New Year holiday falls at a different time in January or February each year means that data for these two months is always weird. Businesses tend to cram trade orders or borrowing in before the holiday—unless they postpone that cramming until after. That’s why interpreting those months’ data is about as precise as entrails-divination.

Even accounting for these distortions, February exports dropped at least 1%, while imports jumped something like 10%, even as imports of iron ore fell. Rather than signaling a fundamental shift, this could simply reflect the response to the PBoC’s currency-fiddling. How? Traders often use fake export orders to bring money into China, and fraudulent import orders to sneak money out and convert it to dollars. So it stands to reason that imports would leap as dollar-demand picked up.

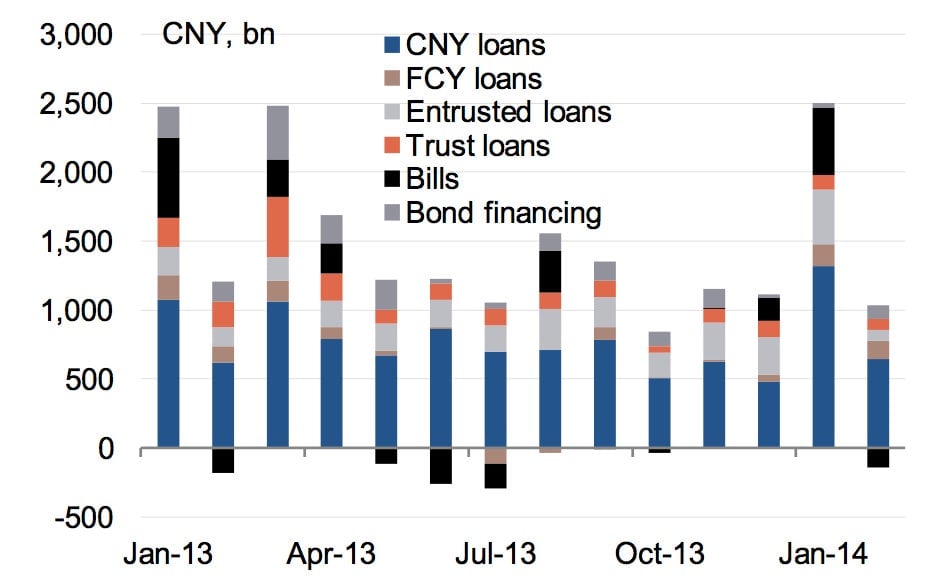

While the same distortions that affect trade also scramble credit data, at least part of February’s unexpected drop in financing can also be explained by the yuan’s withering. In February, the bottom dropped out on the credit measures that contribute to shadow banking. Lending through those channels accounted for only 1% of total financing last month, compared with 28% the previous month, according to calculations by Bernstein Research.

That might be because demand started vanishing mid-month. When Chinese traders bet on the yuan strengthening by borrowing dollars and switching them to yuan, they only stand to turn a small profit by putting those yuan in a Chinese bank account. They can profit like crazy, however, if they invest in off-balance-sheet wealth management products, investment vehicles that banks market to retail customers that securitize risky loans. These often offer rates in the 6-10% range—much more than the 3% or so you can get holding yuan as a bank deposit.

We know that in the last week of February, speculative traders had to swap yuan for dollars to cut their losses on loans. You can’t invest in WMPs with dollars—which means that a lot of the usual shadow-banking funding dried up in the rush to dollars. That drop in demand could further depress interbank rates.

So are we seeing a new phase in China’s monetary policy? Not really, says the Conference Board’s Polk, who thinks that the sell-off of yuan could mean more deposits, creating a larger lending base for banks. “I’m still not convinced January and February [lending] numbers are the nail in the coffin of overly expansive credit conditions,” he says, adding that we’ll have to wait until March to get a better sense.

That means fears that some sort of panic is afoot in China are probably overblown. But the real worry—“Japanese-style deflation,” as Charlene Chu, an expert on shadow banking, put it—looms just as large as before, says PIIE’s Borst.

“The Japan scenario for China is a real risk,” he says. “If non-performing loans are not resolved and instead are rolled over, this will reduce the ability of banks to make future loans to more productive enterprises. Growth will slow down if an increasing share of credit is claimed by inefficient firms.”